Maintaining consistent trade discipline requires clear rules on risk exposure. One of the most practical tools for implementing those rules is a position sizing calculator. These calculators help traders determine how much capital to allocate to a single trade based on predefined risk parameters. By relying on objective inputs rather than instinct, traders reduce emotional bias and improve long-term consistency. In competitive financial markets where price movements can be rapid and unpredictable, structured decision-making provides a measurable advantage. The position sizing process forms a bridge between abstract risk management theory and daily trading execution.

Understanding Position Sizing

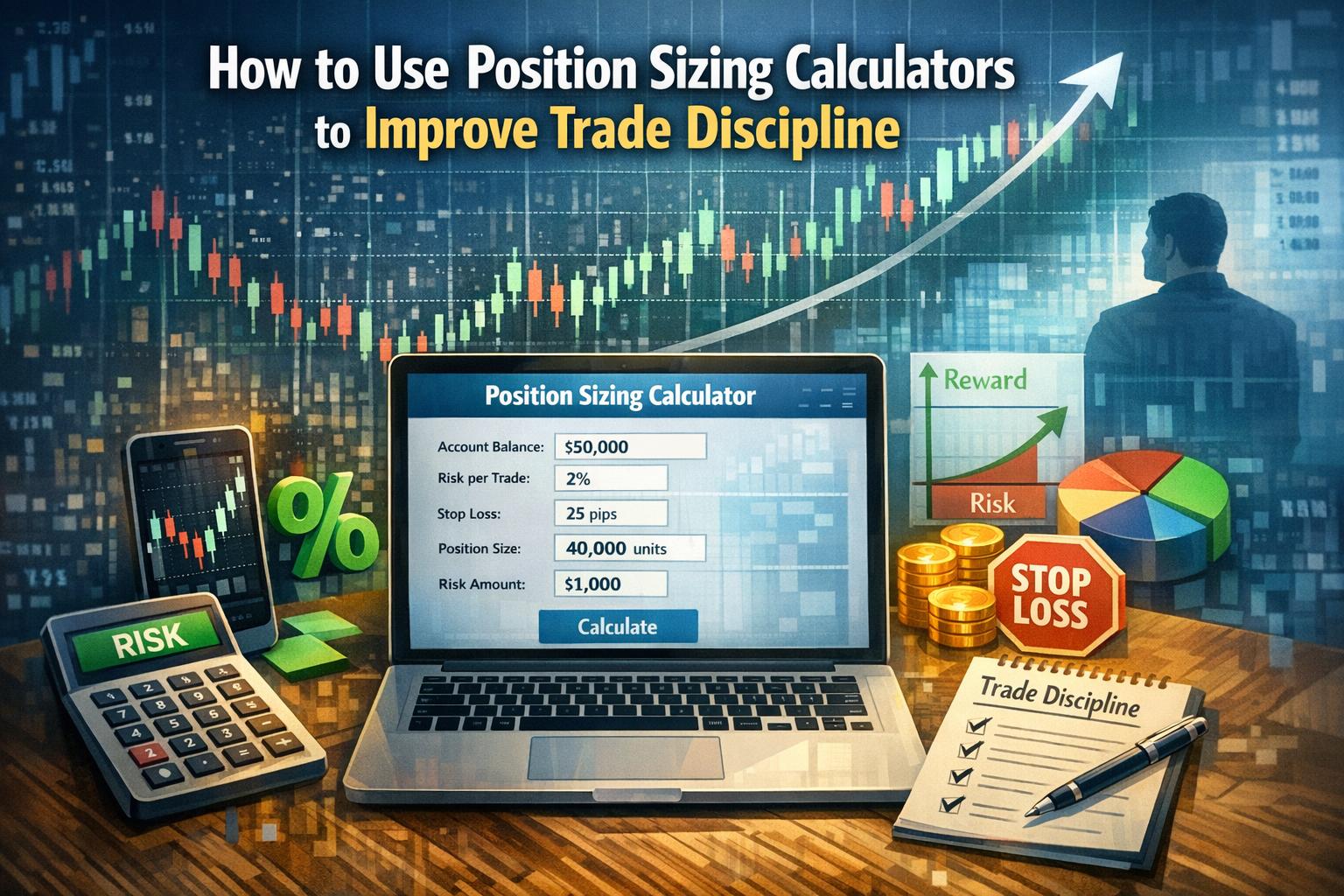

Position sizing refers to the process of determining how many units of an asset to buy or sell in a single trade. The calculation typically considers account balance, risk percentage per trade, entry price, and stop-loss level. This approach ensures that no single trade has a disproportionate impact on overall capital. Without structured sizing, trade exposure can vary significantly from one position to another, leading to inconsistent performance and avoidable drawdowns.

At its core, position sizing translates a percentage of account equity into a defined monetary risk. If a trader manages an account of $50,000 and decides to risk 1% per trade, the maximum acceptable loss equals $500. The next step is to determine how far the stop-loss is placed from the entry price. If that distance represents $5 per share in a stock trade, the calculator divides the allowable risk ($500) by the risk per share ($5), resulting in a position size of 100 shares. This systematic approach ensures that if the stop-loss is triggered, the loss remains within the predefined threshold.

Many brokerage platforms integrate calculation tools directly into their order entry systems. Independent financial websites also offer specialized calculators capable of adjusting for various asset classes. Regardless of format, the purpose remains consistent: convert risk tolerance into precise trade size.

The Mathematical Foundation of Risk Control

The effectiveness of a position sizing calculator is grounded in basic probability and capital management principles. Trading outcomes occur in sequences, and even strategies with positive expectancy experience periods of losses. If risk per trade fluctuates widely, sequences of losses can cause disproportionate equity reductions. A structured percentage-based model stabilizes this exposure.

Consider a scenario in which a trader risks 5% of capital on each trade. A series of ten consecutive losses would reduce account equity by nearly half. In contrast, risking 1% per trade under the same conditions results in a substantially smaller drawdown. Because capital preservation is essential for continued participation in the market, limiting per-trade risk supports long-term sustainability.

Position sizing also interacts directly with the concept of expectancy. If a strategy produces an average return greater than its average loss over a sufficiently large sample of trades, consistent sizing allows that statistical edge to manifest. Irregular trade allocation, by comparison, can distort results and make evaluation more difficult.

How Calculators Reinforce Trade Discipline

Trade discipline depends on consistent execution. A position sizing calculator creates a structured environment where each trade follows predefined criteria. Instead of deciding trade size impulsively, the trader inputs measurable data such as account equity and stop distance. This reduces the likelihood of increasing position sizes after losses or overcommitting capital following profitable periods.

The discipline derived from calculators also extends to stop-loss placement. Because trade size depends directly on the chosen stop-loss distance, modifying the stop requires recalculation. This interdependence promotes deliberate planning before order placement. Traders are encouraged to identify logical exit levels based on market structure rather than adjusting them arbitrarily.

Furthermore, predefined risk limits reduce the influence of short-term performance fluctuations. A trader experiencing a drawdown may feel pressure to recover losses quickly by allocating larger capital amounts. A calculator, when used consistently, prevents such deviations from established parameters. The result is a standardized exposure pattern that aligns with the original trading plan.

Core Inputs in a Position Sizing Calculator

Most calculators require four central inputs: account balance, risk percentage, stop-loss distance, and asset specifications.

Account Balance represents total trading capital or, in some cases, available free margin. Accurate reporting of this figure is essential because miscalculations may lead to unintended exposure. Some traders update account balance after every closed trade, while others evaluate it at fixed intervals. The key objective is maintaining consistency in calculation methodology.

Risk Percentage defines how much of the account a trader is prepared to lose on a single position. Common values range from 0.5% to 2%, depending on trading style, volatility of the asset, and personal risk tolerance. Lower percentages generally correspond with higher trading frequency or more volatile markets.

Stop-Loss Distance measures the difference between entry and protective exit levels. This value may be expressed in dollars, ticks, pips, or percentage terms, depending on the instrument. The precision of this figure is critical, since misjudging volatility or market structure can result in either premature exits or excessive exposure.

Asset Specifications include contract size, tick value, or lot size. For example, in futures markets, each contract represents a standardized quantity with defined tick values. Foreign exchange trading often involves lot-based systems where currency pairs have varying pip valuations. Advanced calculators incorporate these specifications automatically, reducing manual error.

Adjusting for Leverage and Margin

Leverage allows traders to control large nominal positions with relatively small capital commitments. While leverage increases capital efficiency, it does not alter the fundamental principles of risk management. A position sizing calculator ensures that leverage amplifies exposure within predefined boundaries rather than expanding it beyond acceptable limits.

For instance, a trader using 10:1 leverage can open a position worth $100,000 with $10,000 in margin. Without proper sizing, the potential loss could exceed planned thresholds. By incorporating stop distance and allowable risk percentage into calculations, the trader ensures that leveraged exposure aligns with account risk constraints. This disciplined approach distinguishes structured leverage use from uncontrolled speculation.

Integrating Calculators into a Trading Plan

A position sizing calculator should function as an integral component of the trading workflow. Before entering a trade, the trader identifies the setup, determines the technical or fundamental rationale, establishes the stop-loss point, and calculates the corresponding position size. Only after these steps are completed should the order be placed.

Embedding this sequence into a routine reduces variability in decision-making. Over time, the repetition of standardized preparation fosters procedural consistency. Some traders automate this process within algorithmic systems, while discretionary traders may rely on spreadsheet templates or platform-based tools. In both cases, the principle remains identical: trade size derives from risk parameters, not from profit expectations.

Incorporating position size records into a trading journal further reinforces discipline. Documentation enables performance analysis based on true risk exposure rather than nominal returns. For example, a 2% account gain achieved with 1% risk reflects a different risk-adjusted profile than the same gain achieved with 3% exposure.

Drawdown Management and Equity Fluctuations

Drawdowns are inevitable in trading. A percentage-based position sizing model naturally adjusts exposure during both growth and contraction phases. As account equity increases, allowable risk in monetary terms expands proportionally. Conversely, when losses occur, subsequent trade sizes decrease. This automatic adjustment stabilizes the rate of equity change.

Such scaling contributes to survival through adverse periods. Rather than maintaining constant trade size regardless of equity fluctuations, which may accelerate losses during drawdowns, disciplined sizing aligns exposure with current capital conditions. This proportional reduction supports capital preservation and facilitates recovery.

Psychological Effects of Structured Sizing

Although position sizing is a quantitative process, its benefits extend into cognitive aspects of trading. Predetermined risk limits reduce uncertainty regarding worst-case outcomes. When traders know in advance the exact capital amount at risk, decision-making becomes more structured. There is less ambiguity about potential loss magnitude.

The reduction of ambiguity can improve adherence to stop-loss orders. Traders who risk excessive amounts may hesitate to close losing positions, hoping for reversal. By contrast, when loss levels are calculated within acceptable boundaries, executing exits becomes a procedural step rather than a reactive decision.

Common Implementation Errors

Despite availability of calculators, some traders override calculated values. Increasing trade size to meet desired profit projections distorts risk-reward relationships. Similarly, failing to recalculate after modifying stop levels undermines the purpose of structured sizing.

Another frequent issue involves inconsistent risk percentages. Adjusting exposure based on recent performance introduces variability unrelated to strategy quality. While long-term adjustments to risk parameters may be appropriate, they should be data-driven and implemented systematically rather than in response to isolated outcomes.

Errors also emerge when traders neglect transaction costs or slippage in volatile markets. Although these factors may appear minor individually, repeated discrepancies between theoretical and executed risk can accumulate. Advanced planning should account for such variables where relevant.

Long-Term Stability Through Consistent Exposure

Position sizing calculators translate risk management principles into repeatable action. By defining exposure limits for every trade, they create a stable operational framework. Consistency in trade allocation supports accurate performance evaluation and reduces the probability of catastrophic loss.

Over an extended series of trades, structured sizing allows strategy characteristics to manifest without distortion from irregular exposure. Capital growth, when achieved, reflects measured expansion rather than episodic overcommitment. This alignment between planning and execution forms the basis of disciplined trading practice.

When integrated into daily workflow and upheld without exception, a position sizing calculator becomes more than a numerical aid. It serves as a mechanism for maintaining proportional risk, preserving capital through varied market conditions, and sustaining the operational consistency required for long-term participation in financial markets.